May 2026 Rental & Real Estate Market Update Redding, CA

2026 Housing Dilemma: Renting vs. Selling Explained

For decades, buying a home was considered the cornerstone of building wealth. Your parents probably told you that renting is "throwing money away." But in 2026, that advice deserves a serious second look. Interest rates, housing prices, and the way people live and work have all shifted in ways that make this a genuinely complicated question.

Home prices in most major cities remain elevated compared to pre-pandemic levels. While the frenzy of 2021 and 2022 has cooled, affordability is still a challenge for many first-time buyers. Mortgage rates have stabilized but are not back to the historic lows we saw years ago, which means monthly payments on a new home purchase are considerably higher than they were for people who bought a few years back. On the rental side, competition in many urban markets has softened slightly as new apartment supply came online in 2024 and 2025. That means renters in some cities have more leverage and better options than they did a couple of years ago.

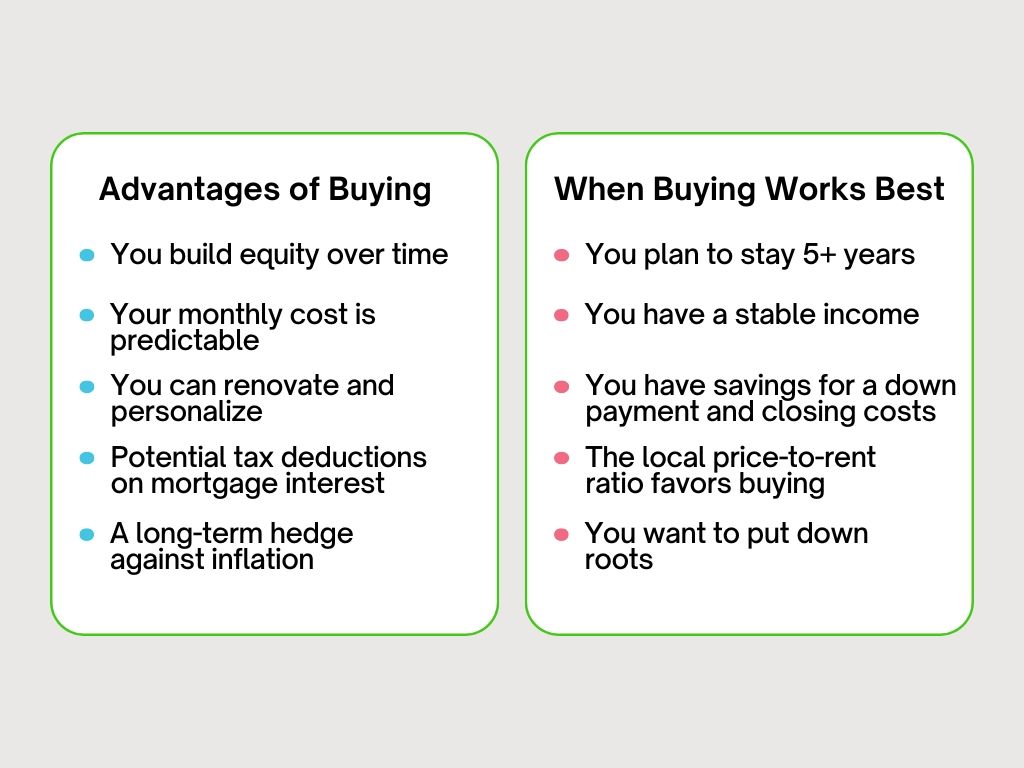

Buying a home still makes strong sense under the right conditions. Here is when it tends to work in your favor.

Equity is the big one. Every mortgage payment chips away at what you owe, and if the property appreciates over time, you are building real wealth. A renter does not have that. But the catch is that this only works if you stay long enough. Buy and sell within two or three years and you may actually lose money after factoring in closing costs, agent fees, and the interest-heavy early years of your mortgage.

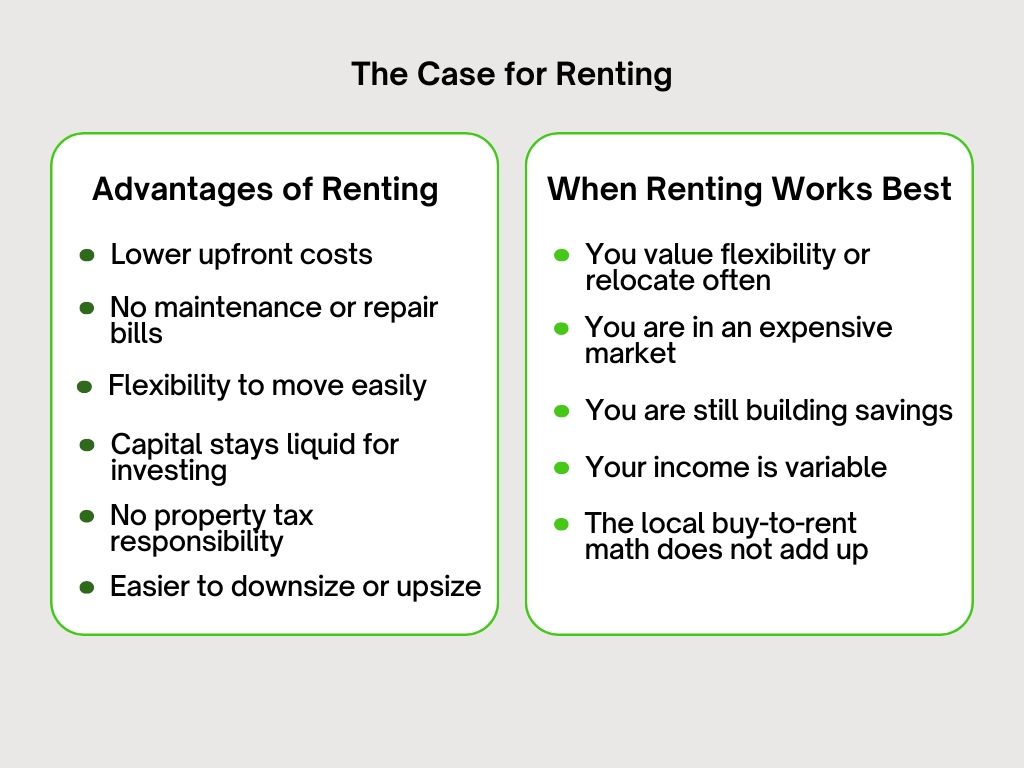

Renting has gotten an unfair reputation. In many situations in 2026, it is genuinely the smarter financial move.

First-time buyers sometimes underestimate what comes after the purchase. Beyond the mortgage, you are responsible for property taxes, homeowner's insurance, HOA fees if applicable, and all maintenance and repairs. A leaking roof, a broken HVAC system, or a flooded basement is now your problem. Financial advisors often suggest budgeting 1 to 2 percent of your home's value annually for upkeep. On a $400,000 home, that is $4,000 to $8,000 a year that renters simply do not have to think about.

The old argument that renters cannot build wealth is simply not true anymore. If you rent a more affordable place and invest the difference, including the money you would have tied up in a down payment, you can grow meaningful wealth through the stock market or other investment vehicles. This strategy only works if you are actually disciplined about investing that money rather than spending it. But for people who can stick to it, the numbers can be competitive with homeownership, especially in expensive markets.

Money is not the only factor. Owning a home gives many people a sense of stability, community, and freedom to make the space their own. If you have kids and want to stay in one school district, or if you are ready to put down roots, those are real and valid reasons to buy even if the pure financial case is close. On the other hand, if your job involves travel, if you are not sure about a city yet, or if you simply value the freedom to pick up and move, renting is not a compromise. It is a lifestyle choice that aligns with your priorities.

Buy if:

You plan to stay at least five years, you have solid savings and stable income, your local price-to-rent ratio is below 20, and you are ready for the responsibilities of ownership.

Rent if:

You are in an expensive market, you value flexibility, you are still building your financial foundation, or the monthly cost of owning a comparable home is significantly higher than renting.

There is no universal answer because there was never supposed to be one. The decision is deeply personal and depends on your market, your finances, and where you are headed in life. What matters is that you run your own numbers honestly, not the numbers your emotions want to see.

Talk to a fee-only financial advisor if you can, do your research. And then make the decision that fits your real life, not the one that sounds right at a dinner party.

Share this post with a friend!

Disclaimer: The content on this blog is for informational purposes only and is not intended as legal or advice. Consult with a qualified professional for specific advice.

Anderson, Bella Vista, Cottonwood, Happy Valley, Igo, Keswick, Lake California, Millville, Mountain Gate, Oak Run, Ono, Palo Cedro, Redding, Shasta County, Old Shasta, Shasta Lake,

Authority Property Management Inc. in Redding, CA is a licensed Property Management Company and Rental Agency. We offer comprehensive real property management services in Shasta County and surrounding areas. Our expertise includes managing rental properties, single-family homes, apartments, and commercial properties.

Contact Us Today For Expert Property Management Services In Redding, CA!

2025 Authority Property Management Inc., Redding, CA. All Rights Reserved. View Our Privacy Policy